See exactly what a bank sees before you apply. Spendle helps you clean up the red flags, gather your savings evidence, and share a tidy report with your broker, so you can walk in calm and prepared.

Read-only bank connection via Akahu. Your data is stored securely.

What banks actually look at

The five things a lender checks

Once you can see your application the way a bank does, the whole thing gets a lot calmer. Here is what they weigh up.

How does your income stack up?

Banks want to see income that is steady and reliable. For salaried work that usually means recent payslips; if you are self-employed they often look at one to two years of financial statements. Predictable income is easier to lend against.

What do your real living expenses look like?

Banks review your actual bank statements, not just the expenses you declare. The daily coffees, subscriptions and weekend takeaways all count, because the bank is working out how much is genuinely left over each month. Tidy, well-categorised statements help your case.

What liabilities are you carrying?

Every commitment reduces how much a bank will lend. That includes car and student loans, and two that catch people out: credit card limits (often counted in full even at a zero balance) and Buy Now Pay Later use, which can read as a sign that day-to-day spending is tight.

What does your credit history say?

Banks check your credit record to see how you have handled credit before. Missed payments, defaults and lots of recent applications can leave a mark. The fix is usually simple: pay on time, and give any blemishes time to age.

Where is your deposit coming from?

How much deposit you have changes everything, including your interest rate. Banks also want to see the deposit is genuinely yours, whether it is savings, KiwiSaver, or a documented gift, and a steady savings record is strong evidence you can manage repayments.

Two numbers worth knowing

As general guidance, not advice: lending rules limit borrowing to around six times your gross income (your DTI), and banks often stress-test your loan at around an 8% serviceability rate rather than today’s actual rate. The exact figures move over time.

How Spendle helps

Everything you need, ready to share

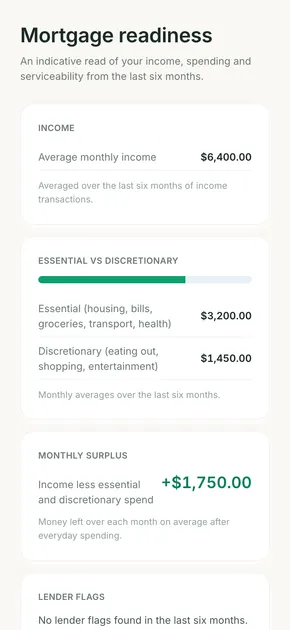

A readiness reportA clear summary of where you stand, built from your real statements, ready to share with your broker.

A red-flag pre-checkSpot the things a bank might pause on, like a high credit card limit or regular BNPL, with time to tidy them up.

Savings evidenceShow a steady savings record and a growing deposit, the way a lender likes to see it.

An indicative DTI snapshotA rough sense of your debt-to-income position, so there are fewer surprises in the meeting.

A read-only broker share linkShare a tidy, read-only view with your broker or adviser. No screenshots, no spreadsheets.

Spendle provides information to help you prepare. It is not a lender or a licensed financial adviser, and the figures it shows are indicative. Lending decisions, rates and criteria are set by banks and can change. For advice tailored to your situation, talk to a mortgage adviser or your bank.

Common questions

What banks look at, in detail

How does your income stack up?

Banks want to see income that is steady and reliable. For salaried work that usually means recent payslips; if you are self-employed they often look at one to two years of financial statements. Predictable income is easier to lend against.

What do your real living expenses look like?

Banks review your actual bank statements, not just the expenses you declare. The daily coffees, subscriptions and weekend takeaways all count, because the bank is working out how much is genuinely left over each month. Tidy, well-categorised statements help your case.

What liabilities are you carrying?

Every commitment reduces how much a bank will lend. That includes car and student loans, and two that catch people out: credit card limits (often counted in full even at a zero balance) and Buy Now Pay Later use, which can read as a sign that day-to-day spending is tight.

What does your credit history say?

Banks check your credit record to see how you have handled credit before. Missed payments, defaults and lots of recent applications can leave a mark. The fix is usually simple: pay on time, and give any blemishes time to age.

Where is your deposit coming from?

How much deposit you have changes everything, including your interest rate. Banks also want to see the deposit is genuinely yours, whether it is savings, KiwiSaver, or a documented gift, and a steady savings record is strong evidence you can manage repayments.

Get mortgage ready, the calm way.

Start free, then upgrade to Pro to build your readiness report. Cancel any time. Spendle is on iPhone, Android and the web.